Fix and Flip Calculator —

Profit, MAO, and the 70% Rule.

Run a flip in 60 seconds. Real hard money cost, time-weighted holding costs, honest MAO. Built by an active flipper, not a hard money lender trying to fund your deal. No signup to run a deal.

Defaults: 90% purchase + 100% rehab on hard money, 6% sale commission, 30 days on market, $35k desired profit, 1% TRR buffer. Sign up to override every assumption.

What You're Seeing Above is ~10% of the Product.

The free preview runs the same math as the full tool — it just exposes a fraction of the inputs and none of the operational features. Here's what the full Value Add Calculator ships with:

No card charged until day 15. Cancel any time.

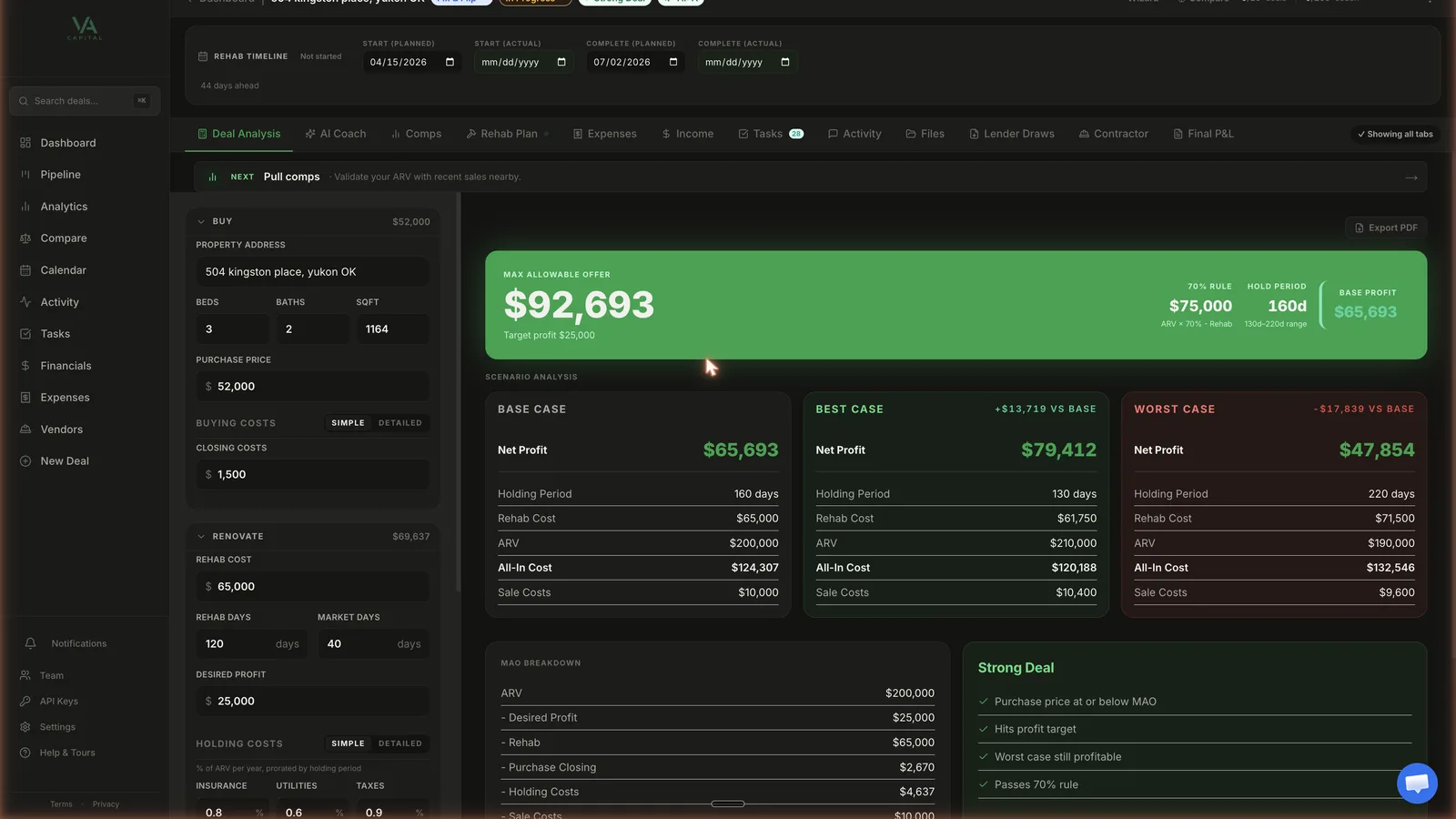

The Actual Deal Page You Get After Signup.

Sidebar nav · AI Deal Grade · full input panel · live results · scope of work · comps · expense tracker · tasks · activity feed · branded PDF export.

How Fix-and-Flip Math Actually Works

A flip is one math problem. Sale price minus every dollar you spent to get there equals profit.The trap is that operators dramatically underestimate the "every dollar you spent" side.

Purchase. Acquisition price plus closing costs plus hard money points and fees. If you are using a 90% LTV hard money loan with 2 points and $1,500 in fees, the loan itself costs you ~$3,500 before a single contractor shows up. Most retail flip calculators ignore this entirely.

Rehab. Whatever your scope of work prices out at. Then add 10–15% because you will find something. Roof rot. Galvanized pipe. A foundation crack you missed at the walkthrough. I had a $40k rehab become $62k by month four on a flip in OKC because the bathroom tile demo exposed an old leak nobody priced in.

Holding costs.The line item that kills flips. Hard money interest accrues every single day from close to payoff. On a $150k loan at 11% for 120 days that is about $5,400 in pure interest. Add taxes, insurance, utilities, and lawn care over the same period. Your "90-day flip" that becomes a 180-day flip just doubled the holding cost.

Sale costs. 6% commission, $2,000 in seller closing, sometimes a buyer concession, and a 1% TRR (transaction risk reserve) buffer for the surprise — appraisal gap, repair request, escrow shortage. On a $235k ARV that is ~$16,400 off the top before you net a dime.

Net profit. ARV minus all of the above. Most operators run the math without holding costs and HM interest and think they have a $50k profit. The real number is $32k. Two months over schedule and it is $19k. Three months and it is breakeven.

The math problem at the center: buy low enough that even if rehab overruns and the market softens 5%, you still net real profit. That is what the MAO field above is telling you. If your offered price is above MAO, you are pre-eating margin.

What This Calculator Does That Free Ones Don't

Search "fix and flip calculator" on Google. Pages 1–3 are lender lead-gen pages. RehabFinancial, FirstEquityFunding, New Silver, Kiavi. The calculator is a top-of-funnel for their loan product. The math is fine, but the whole experience is engineered to push you into a quote form.

Here is what this one does differently:

- Real hard money cost. Purchase loan accrues interest on the full balance from day one. Rehab loan disburses incrementally — we apply the standard 50% draw-schedule approximation so you are not paying interest on $55k of rehab money you have not actually drawn yet. Points and fees are itemized up front.

- Time-weighted holding costs. Insurance, utilities, and taxes are multiplied by your rehab days plus market days. Not a flat percentage. Not "6 months" locked. Edit the rehab-days input and watch holding cost move in real time. That is how you stress-test what happens when a project goes long.

- Honest 70% rule application. The MAO field is calculated against your actual cost structure and desired profit, not the back-of-napkin 70%-of-ARV-minus-rehab shortcut. The shortcut works on a phone call. It does not work on a deal you are about to fund.

- Best-case / worst-case scenarios. Inside the full Value Add Calculator (gated, free trial), every flip runs a base/best/worst scenario simultaneously. ARV ±5%, rehab ±10%, days ±60. The deal that pencils only in the base case is the deal that kills you in the worst case.

- No lender capture. Nothing on this page asks for your email to get the calculator. You can use it forever without signing up. Signup unlocks deal management — scope of work, expense tracking, draw requests — not the math.

Translation: when you sign up and run the same deal inside the full Value Add Calculator, the numbers don't move. The engine up top is the engine inside.

What You Get When You Sign Up

The free calculator runs one deal. The paid tool runs every deal in your pipeline plus the rehab itself.

Solo $59/mo · Pro $149/mo · Team $299/mo · No card charged for 14 days

Built by an Active Flipper

I'm Cam Burke. I run Tuff Homes, an active flip company in Oklahoma City, and operate 70+ rental units through Tuff Holdings. The first flip calculator I built was a Google Sheet — and it broke every time a deal had real hard money cost, real holding cost, or a rehab that ran long.

Every fix-and-flip calculator on the internet is built by one of two groups: hard money lenders running lead-gen, or software companies that have never closed a flip. The first group inflates the rosy outcome. The second group ignores half the cost lines because the founders haven't felt them yet.

This one is the calculator I run my own deals through. Holding costs are time-weighted because I've eaten a 30-day delay and watched $4k disappear. Hard money cost is honest because I've underwritten a deal at 10% interest and closed it at 11.5% after the lender re-priced.

If you sign up, the full version does AI scope-of-work generation from property photos, tracks rehab spend against budget, generates draw request PDFs your hard money lender will actually accept, and rolls everything into a pipeline dashboard so you can see all your live deals in one place.